As girls proceed to broaden their presence within the company workforce, their function in managing cash is evolving alongside it. In an area historically dominated by males, girls are more and more stepping in—investing, evaluating choices and interesting with monetary recommendation. Monetary decision-making, as soon as seen by way of a gendered lens, is now rising as a sensible necessity fairly than an outlined function.From mutual funds and equities to safer devices, participation is broadening. However whilst involvement grows, the diploma of impartial management—notably in areas like tax planning—stays uneven, suggesting a transition that’s nonetheless below means.So, let’s dive deep into how a lot girls get entangled in funding and tax planning.

Participation grows – with recommendation

Girls’s participation in India’s workforce presents a combined image; rising on the macro stage however nonetheless restricted inside company India. In keeping with a report from the Press Data Bureau (October 2025), the feminine labour pressure participation price has almost doubled from 23.3 per cent in 2017–18 to 41.7 per cent in 2023–24, signalling a broader shift in the direction of inclusion. Nevertheless, company information tells a extra constrained story. A report by the CFA Institute reveals that ladies account for just below one-fifth of the workforce in listed corporations, with their share slipping barely to 19.4 per cent from 19.6 per cent between FY 2022–23 and FY 2024–25, regardless of large-scale hiring. Collectively, the figures counsel that whereas extra girls are getting into the workforce total, their illustration in formal company roles, and development inside them, stays uneven.The shift isn’t just anecdotal. Trade specialists level to a gradual rise within the variety of girls getting into formal funding channels, aided by fintech platforms, simplified onboarding and larger consciousness round monetary independence.To get the final girls perspective, a small survey of 30respondents performed by TOI mirrored on this development. Most respondents indicated that they actively make investments their cash, however typically with inputs from monetary advisors or members of the family. This factors to a extra nuanced actuality: girls should not absent from decision-making, however decision-making is often collaborative fairly than absolutely impartial.

Desire for stability, however diversification is rising

Whereas participation has elevated, funding decisions nonetheless present a tilt in the direction of comparatively safer or acquainted devices, akin to fastened deposits and conventional financial savings merchandise. On the identical time, publicity to market-linked choices like mutual funds and equities is progressively rising.This displays a mixture of danger consciousness, earnings patterns and long-term monetary priorities, fairly than a easy reluctance to take a position, based on Sanaa Zia Khan, Director at Centricity Abroad Monetary Distribution Pvt. Ltd, founding member of INVICTUS, Centricity WealthTech.“Girls buyers are typically comparatively conservative of their asset allocation, typically prioritising capital safety and the safekeeping of financial savings over long-term wealth creation. In lots of households, the duty for pursuing higher-growth investments nonetheless largely falls on male members of the family. Whereas a balanced danger urge for food is necessary, very restricted publicity to growth-oriented belongings can result in under-allocation of assets and will end in lacking out on key asset courses,” she advised TOI.“Moreover, in lots of households, main funding selections are nonetheless not actively shared with girls. This typically results in monetary planning that’s incident pushed and never structured. Life occasions akin to profession breaks or caregiving duties additional spotlight the significance of a disciplined monetary construction,” she added.The survey responses additionally confirmed this steadiness, with many members indicating diversified portfolios however a cautious method to danger.As an example, Aanshi Kanaujia, a working skilled in media trade in her 20s, stated she manages her investments independently, with a portfolio spanning mutual funds, fastened deposits and gold, primarily aimed toward long-term wealth creation. Equally, Sakshi Jha, one other media skilled, stated she absolutely manages a diversified portfolio together with equities, mutual funds, fastened deposits and insurance coverage merchandise. Nishu Kathuria, additionally in her 20s, echoed this shift in the direction of impartial decision-making, saying she manages her investments herself throughout mutual funds, gold and actual property, reflecting a rising consolation with diversified, growth-oriented belongings amongst youthful buyers.On the identical time, some respondents highlighted a extra balanced or advisory-led method. Sakshi, a physician in her 30s, stated she manages her investments with steering from household or advisors, specializing in mutual funds and stuck deposits for long-term wealth creation and tax planning. Nevertheless, she avoids getting concerned in total household monetary planning, which she leaves to others.On the different finish of the spectrum, some respondents stated they’ve but to start investing altogether. A instructor in her 30s, advised TOI (anonymously) she doesn’t make investments at current, citing hesitation and concern of potential losses, reflecting how danger notion continues to form participation for a piece of girls.In the meantime, speaking about forms of belongings girls are investing in, Unnati Gala, a model communication specialist, follows a diversified technique spanning equities, gold and actual property, combining wealth creation with sensible objectives like emergency funds and way of life planning.Shuchi, an physiotherapist, invests throughout asset courses – together with equities, mutual funds, fastened deposits and insurance coverage; whereas counting on recommendation to align her portfolio with long-term objectives. Nevertheless, a piece of members nonetheless depends on others for monetary decision-making or has but to start investing. An nameless respondent in her 30s working in enterprise stated she doesn’t actively make investments and leaves monetary selections to members of the family, whereas one other media skilled in her 20s famous that though she has long-term monetary objectives, funding administration is dealt with by others.Throughout responses, even amongst those that don’t immediately handle investments, many indicated that they actively take part in monetary discussions inside their households. This implies that whereas possession of monetary selections should be uneven, consciousness and engagement are steadily rising.

Enhancing monetary outcomes would require stronger monetary literacy, higher entry to skilled recommendation, and larger confidence in long-term investing, enabling girls to play a extra lively function in constructing and managing their monetary portfolios.

Sanaa Zia Khan, director at Centricity Abroad Monetary Distribution Pvt. Ltd. and a founding member of INVICTUS, Centricity WealthTech

Tax planning stays a weak hyperlink

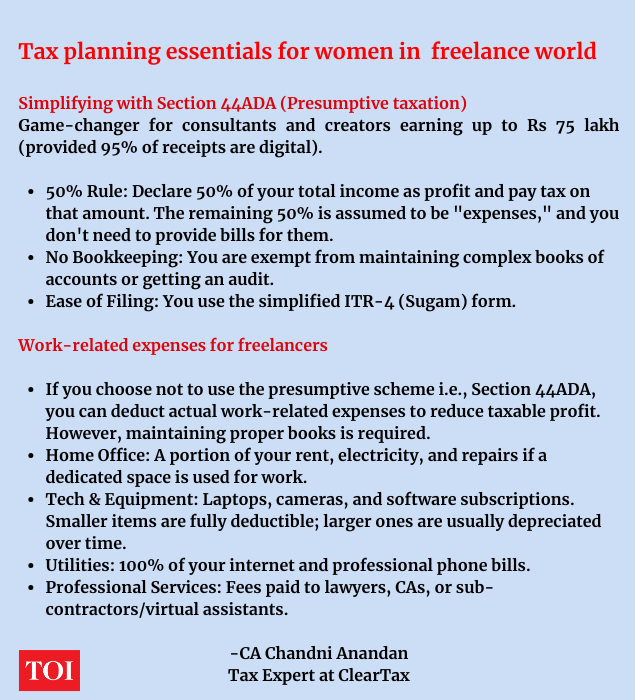

If investing is turning into extra mainstream, tax planning continues to lag behind.Whereas extra girls are taking part in monetary markets and constructing diversified portfolios, tax planning is usually handled as a secondary train; usually addressed nearer to submitting deadlines fairly than as a part of a structured, year-round monetary technique.This hole turns into extra important as work patterns themselves evolve. In keeping with the Financial Survey 2025-26, India’s labour market is present process a structural shift, with a 55 per cent rise in gig employees between FY21 and FY25 and rising participation in self-employment and entrepreneurial actions. Girls now account for almost 28 per cent of the workforce within the unincorporated non-farm sector, reflecting a gradual transfer in the direction of versatile and non-traditional types of work.On the identical time, the share of self-employed girls has risen sharply in recent times, indicating a broader shift away from purely salaried roles .This transition has direct implications for taxation.Chandni Anandan, Tax Professional at ClearTax, advised TOI that transferring from salaried roles to freelancing basically adjustments how earnings is classed, reported and taxed. Freelancers are required to file completely different ITR varieties, account for TDS deductions, and in lots of circumstances, pay advance tax—making compliance extra complicated than for salaried people.Right here’s how she defined the taxation on transitioning from Salaried to FreelancingFor ladies transferring from a salaried job to impartial work, the most important shift is in how earnings is reported and taxed.

- Revenue Classification: Not like a wage, freelance earnings is taken into account and reported below the top “Income and Positive aspects from Enterprise or Occupation.”

- ITR Submitting: You have to file ITR-3 or ITR-4 (Presumptive taxation) as a substitute of the usual ITR-1.

- Tax Regimes: The New Tax Regime is the default. Not like reporting wage earnings the place switching regimes is straightforward, taxpayers with enterprise {and professional} earnings have to file Kind 10-IEA to go for the previous tax regime.

- TDS Consciousness: Shoppers usually deduct 10% TDS below Part 194J on funds exceeding Rs. 50,000 for skilled companies.

She additionally identified that provisions like Part 44ADA can simplify taxation for professionals by permitting presumptive earnings declaration.

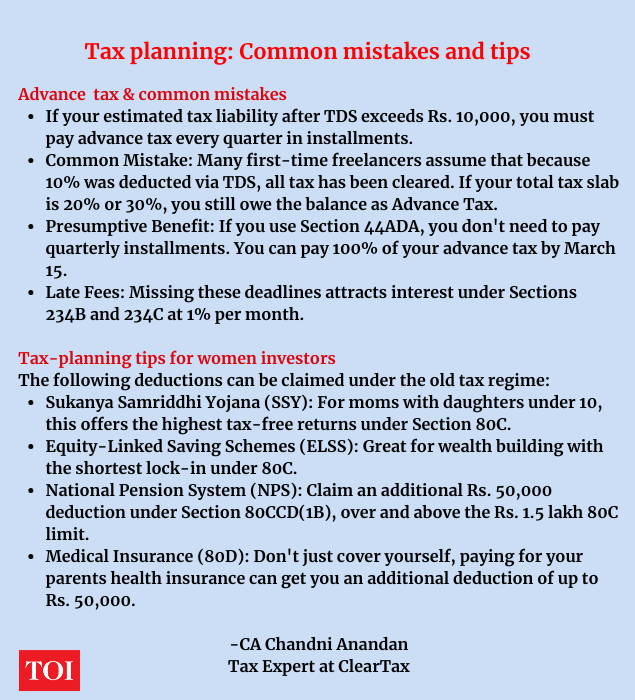

Anandan additionally detailed some frequent errors to concentrate on for straightforward and correct tax submitting like being conscious of final dates and the intricacies round availing the presumptive profit or some deduction advantages girls should be privy to.

In the meantime, amongst survey respondents, solely a small proportion stated they actively plan their taxes by way of the 12 months, whereas the bulk both plan often or assess their tax legal responsibility solely on the time of submitting returns.This sample is seen throughout responses. This sample is seen throughout responses. Prachi Kumari, a PR skilled in her 20s, and Anjali Yadav, a communication specialist in her 20s, each of whom handle their investments independently, had been amongst those that stated they assess taxes solely on the time of ITR submitting.Even amongst those that have interaction extra actively, tax planning is usually periodic fairly than steady. A number of respondents (out of 30) stated they plan “generally”, whereas a smaller phase reported planning yearly with a clearer view of potential liabilities.For a lot of salaried people, tax-saving stays restricted to straightforward deductions or last-minute investments, fairly than a structured, year-round technique. Consultants famous that this could result in missed alternatives for optimising returns and constructing long-term wealth.

Why the hole persists

Regardless of larger participation, a number of structural and behavioural components proceed to form outcomes:

- Restricted early publicity to monetary decision-making: A key issue is restricted early publicity to monetary decision-making. A number of respondents cited lack of monetary information as a main barrier, typically resulting in reliance on members of the family or advisors. One respondent (speaking anonymously) stated she has “grown accustomed to counting on my dad” for monetary selections, reflecting how these patterns can carry throughout generations.

- Family dynamics: Family dynamics additionally proceed to play a job. Whereas many ladies stated they actively contribute to discussions, decision-making continues to be, in some circumstances, delegated. As an example, a professor in her 50s, talking anonymously, stated she depends on household or advisors for managing investments and assesses taxes solely on the time of submitting, reflecting a broader development of partial involvement fairly than full possession.

- Time constraints and competing priorities: Respondents throughout age teams pointed to busy work schedules, caregiving duties and restricted bandwidth as causes for not managing investments or tax planning extra proactively. Behavioural components akin to concern of danger and restricted disposable earnings additionally emerged strongly. A number of members stated issues about potential losses or inadequate funds maintain them again from exploring market-linked devices or extra subtle methods.

- Treating tax planning as compliance fairly than technique: Tax planning itself is usually seen as a compliance train fairly than a strategic device. Many respondents admitted to assessing taxes solely on the time of submitting or “generally” through the 12 months, reinforcing the tendency to method it reactively fairly than as a part of long-term monetary planning.

Collectively, these components contribute to a state of affairs the place girls are getting more and more concerned in investing, however not all the time driving each facet of monetary planning.

A gradual shift in the direction of possession

There are, nonetheless, clear indicators of change.Youthful girls and first-time buyers are displaying larger consolation with digital platforms, systematic funding plans (SIPs) and goal-based investing. Entry to info and ease of execution are serving to bridge a number of the earlier gaps.The survey additionally means that many ladies are searching for recommendation actively fairly than passively following it, indicating a shift in the direction of extra knowledgeable participation.“Younger girls within the workforce are eager about cash in another way. Not simply saving it. Really placing it someplace. Mutual funds, equities, Part 80C, NPS, these conversations aren’t restricted to finance-bro circles anymore. They’re taking place in group chats and remark sections,” stated one of many respondents, Vishakha Nehe, founding father of an influencer advertising and marketing platform.“Tax planning has shifted too. It was a February panic. Now extra girls are constructing their funding selections round annual tax legal responsibility from the beginning, not scrambling when ITR season hits, she added.

From participation to manage

The broader development is clear as girls have gotten a extra seen and lively a part of India’s funding panorama. However the transition from participation to full monetary management, notably in tax planning, stays incomplete.As incomes rise and monetary merchandise change into extra accessible, the following part of this shift will depend upon how far participation interprets into impartial, knowledgeable decision-making.